Most people think escaping debt is all about spreadsheets and interest-rate hacks, yet money pros say the formula is only 20 percent knowledge and 80 percent habit. That means mindset matters more than math. By tweaking how you earn, spend, and invest—while trimming the excess—you can steer clear of high-interest traps and start building real wealth. This guide turns the original tweet’s quick bullets into a deeper, step-by-step playbook. Each section unpacks one practical move you can make today so that bad debt never again controls your paycheck, your plans, or your peace of mind.

1. Know What Makes Debt “Bad”

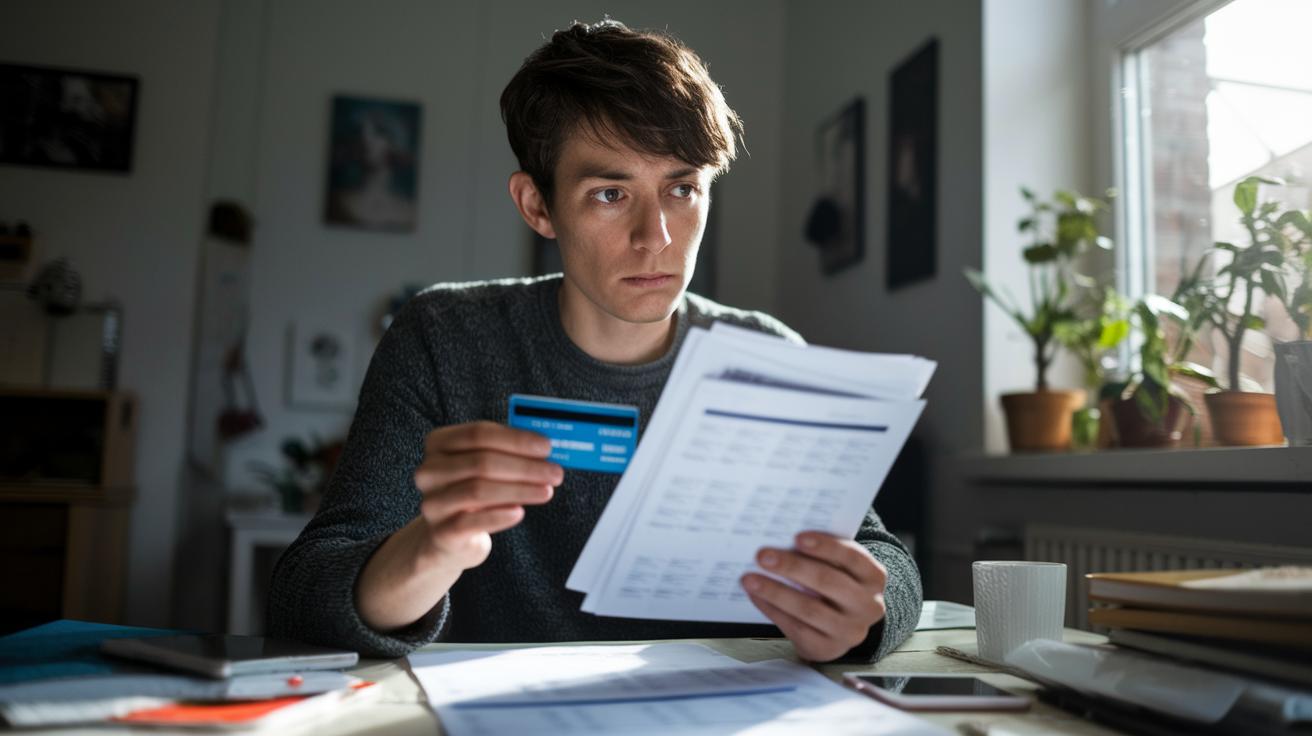

Not every loan is your enemy. Mortgages and carefully used student loans can expand your earning power. “Bad” debt, by contrast, is any borrowing that buys things losing value and charges double-digit interest, think credit cards, payday loans, and installment plans for gadgets you barely needed. The first step is awareness: list every balance, rate, and minimum payment. Rank them from highest APR downward to see which obligations drain you fastest. Recognizing toxic debt clarifies where to attack first and prevents you from justifying that tempting store-card discount at checkout.

2. The 20 Percent: Master the Money Basics

Knowledge may be only one-fifth of the solution, but it’s the lever that moves everything else. Learn how compound interest multiplies both savings and credit charges. Understand amortization schedules so you can predict payoff dates. Get familiar with debt-to-income ratios lenders use to judge your risk. Armed with these facts, you’ll negotiate better rates, refinance strategically, and avoid financial products designed to confuse. Spend an hour a week watching free personal-finance videos, reading blogs, or using calculators. The small education investment pays off with thousands saved in interest over a lifetime.

3. The 80 Percent Habit: Spend Less, Intentionally

Cutting expenses isn’t about deprivation; it’s about alignment. Track every purchase for one month, then highlight buys that didn’t improve your day a week later. Cancel or downsize them. Shift from impulse shopping to planned spending by using a 24-hour wait rule in your cart. Automate bill-pay to dodge late fees, and negotiate recurring costs like insurance or phone plans once a year. Redirect the freed-up cash to accelerated debt payments. Consistency, not perfection, erodes balances: trim $10 here, $50 there, and momentum snowballs faster than you expect.

4. The 80 Percent Habit: Earn More, Expand Your Income Pie

A lean life is easier when the top line grows. Pick a high-demand skill, copywriting, coding, digital design, and monetize it through freelancing platforms or local gigs. Ask for a raise armed with data on your market value, or pursue overtime if your employer offers it. Sell unused items online and funnel proceeds straight toward principal. Even a temporary side hustle delivering groceries or tutoring can generate an extra $300–$500 a month, shaving years off repayment schedules. Remember, every additional dollar earned and applied to debt is a guaranteed, risk-free return equal to your card’s interest rate.

5. The 80 Percent Habit: Invest More, Pay Yourself First

Once high-interest balances are gone, shift the exact payment amount into investments so you don’t inflate lifestyle. Automate transfers to a broad-market index fund or your employer’s retirement plan before the money hits checking. By treating savings as a non-negotiable bill, you harness the same discipline that crushed your debt. Even while repaying, invest modestly if your workplace matches contributions; a 100 percent match beats any quick payoff math. Over decades, compounding grows wealth far beyond what mere frugality can accomplish, ensuring you never need to borrow for emergencies again.

6. Embrace a Lean, Debt-Free Lifestyle for Good

Living lean isn’t a punishment, it’s permission to focus on what truly matters. Choose experiences over possessions, quality over quantity, and community over consumerism. Build an emergency fund covering three to six months of expenses, so surprises don’t send you back to creditors. Review goals quarterly: vacation savings, home ownership, or early retirement. Celebrate milestones creatively rather than by shopping sprees. By making minimalism a habit, you keep financial bandwidth for dreams instead of interest payments. Freedom from bad debt grants you options, resilience, and the peace of mind money can’t buy.

{kind=link}