If your paycheck disappears the moment it hits your account, you’re not alone. But the tweet that sparked this article reminds us of a powerful mindset shift: treat the future as your priciest monthly expense. By funneling cash toward debt elimination, self-improvement, retirement investments, and a rock-solid emergency fund, you build lasting security instead of fleeting comfort. Below, we unpack six practical, future-first strategies—each roughly a coffee break read—to help you redirect more of today’s money toward tomorrow’s freedom.

1. Crush High-Interest Debt First

Debt with double-digit interest is the financial equivalent of running uphill in sand: exhausting and slow. Start by listing every balance, interest rate, and minimum payment. Then use either the avalanche method (highest rate first) or the snowball method (smallest balance first) to attack aggressively. Each debt you eliminate boosts monthly cash flow that can be rerouted to savings and investing. Set payments to autopay on payday so you never "see" the money, and celebrate each payoff milestone to stay motivated.

2. Invest in Your Own Skill Set

Stocks may climb or crash, but upgrading your skills delivers compounding returns no market can match. Allocate a fixed slice of each paycheck to courses, certifications, conferences, or even a few well-chosen books. Focus on capabilities that lift your earning power, coding, project management, public speaking, or industry-specific credentials. Keep a “learning ledger” to track what you spent, what you mastered, and how it influenced promotions or freelance income. When your skills appreciate, so does your salary.

3. Supercharge Retirement Contributions

Missing employer-match dollars in a 401(k) is like turning down free money. Aim to contribute at least enough to grab the full match, then ratchet up 1% a year until you reach 15–20% of income. Don’t stop with workplace plans, open an IRA or Roth IRA for additional tax perks. Automate contributions on payday to make saving invisible, and rebalance annually to keep your asset mix aligned with goals and risk tolerance.

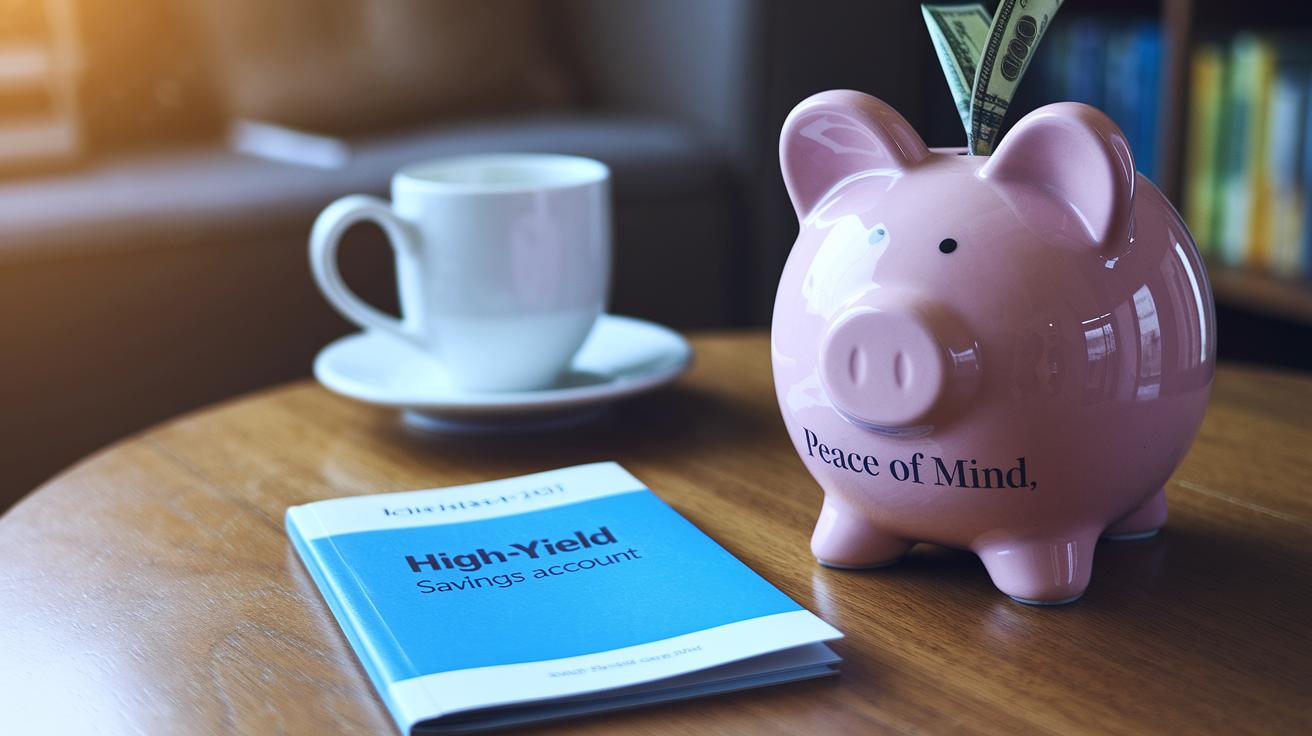

4. Build an Emergency Fund You Can Sleep On

Life loves surprise plot twists: a flat tire, vet bill, or sudden layoff. Stash 3–6 months of living costs in a high-yield savings account that’s separate from everyday spending. Name the account "Peace of Mind" to remind yourself why it exists. Start with a micro-goal, $500, then snowball windfalls, tax refunds, or side-hustle income until the account feels like a financial safety blanket. When emergencies strike, you’ll borrow from yourself, not a credit card.

5. Automate, Track, Repeat

Automation turns good intentions into default behavior. Schedule transfers to debt, savings, and investment accounts the day your paycheck lands. Use budgeting apps or simple spreadsheets to track progress and spot leaks, unused subscriptions, impulse buys, forgotten fees, that can be redirected toward future goals. Conduct a monthly 15-minute "money meeting" with yourself (or your partner) to celebrate wins and set next-month tweaks.

6. Review and Rebalance Every Year

Financial plans aren’t set-and-forget. Revisit insurance coverage, beneficiary designations, and investment allocations annually, or after major life events like a new job, marriage, or move. Check whether you can refinance loans at lower rates, bump retirement contributions, or raise your emergency-fund target. Small course corrections today prevent costly detours tomorrow. Remember: your largest expense should always be the one that buys you the most freedom, your future.

{kind=link}